In the Markets: Oil and Gas Sector Insights

Authors

Neville Jugnauth

Neville Jugnauth

Derek Flaman

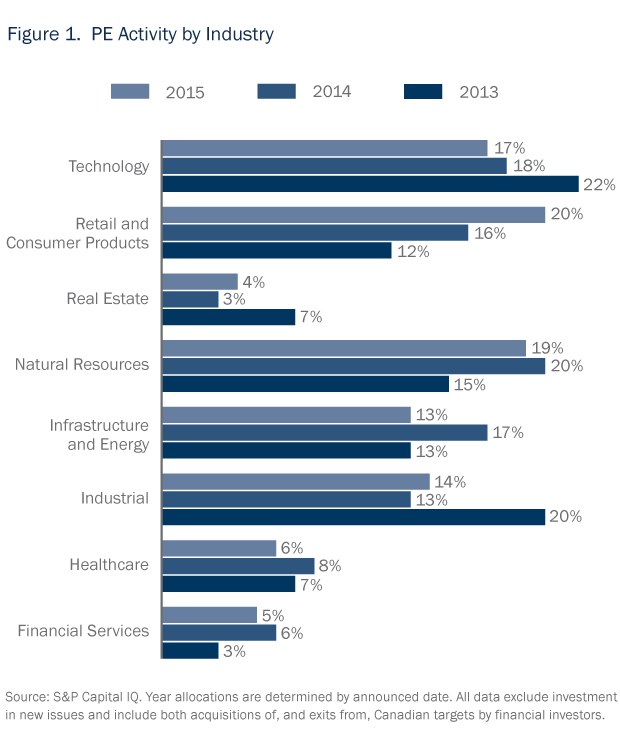

Domestic energy-sector M&A in Canada saw a significant decline in the number of transactions in 2015 as private equity increasingly pursued dealmaking in the Canadian retail and consumer products sector, alongside steady activity in technology, industrial and natural resources sectors (Figure 1).

The decline in energy-sector M&A was largely due to weak industry fundamentals and depressed public company share prices that often made buy side and sell side expectations difficult to reconcile. This was compounded by market uncertainty about the potential impacts of policy initiatives of the recently elected provincial NDP government in Alberta—initiatives that include a provincial energy-sector royalty review, a higher corporate tax environment and new commitments to climate change legislation. With the Alberta government having released the results of its royalty review in late January 2016 and deciding largely to maintain the existing royalty structure, some of this uncertainty should be reduced.

Market access continues to be a significant concern for the industry given the political headwinds that have impacted proposed pipeline projects to date. In early February, in his first visit to Alberta since assuming office, Prime Minister Trudeau delivered a message of federal political support for opening up markets for Alberta energy through new pipelines; however, the message fell short of providing assurances regarding new pipeline approvals, instead emphasizing the need for thorough regulatory review without undue political interference.

A rise in energy-sector deal activity is anticipated in the coming year. With the market adjusting to the realities of a more pronounced oil price decline that isn’t expected to recover substantially in the short term, capital budgets have been slashed and distressed companies have had few options to consider other than asset dispositions or other M&A strategies to address overleveraged balance sheets and the resulting concerns of lenders, or to raise capital for higher priority projects. In addition, there has been robust activity with respect to midstream oil infrastructure asset opportunities as producers look to monetization strategies around the infrastructure they own in order to address balance sheet liquidity issues. Both financial buyers and well-capitalized strategic buyers will look to take advantage of these opportunities. A relatively low Canadian dollar is also expected to motivate foreign buyers hoping to find attractive investments in the current environment in Canada.

To discuss these issues, please contact the author(s).

This publication is a general discussion of certain legal and related developments and should not be relied upon as legal advice. If you require legal advice, we would be pleased to discuss the issues in this publication with you, in the context of your particular circumstances.

For permission to republish this or any other publication, contact Janelle Weed.

© 2025 by Torys LLP.

All rights reserved.