Canadian infrastructure and energy M&A outlook

Authors

Infrastructure and energy assets remain top of mind for buyers and sellers at the outset of 2025. There is growing demand for infrastructure and energy projects to meet rising energy needs, pointing to continued M&A opportunities within this space.

This article shares important data points from recent Canadian infrastructure and energy M&A activity, highlighting trends that are expected to shape the deal environment for the remainder of the year.

Sizing up Canadian infrastructure and energy M&A

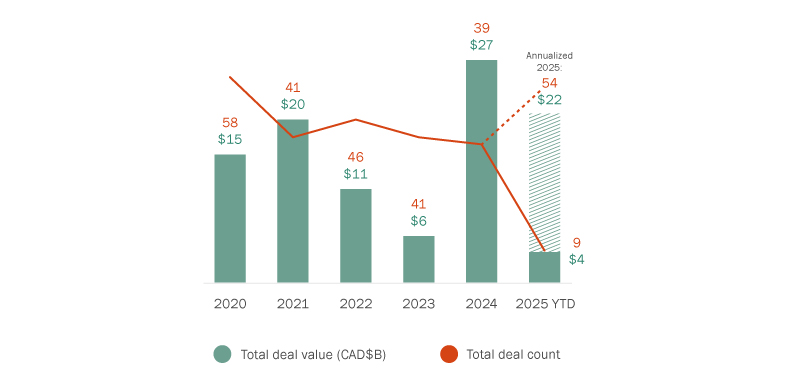

M&A activity in the Canadian infrastructure and energy projects space remains strong, with 39 deals in 2024 (see Figure 1), reflecting consistent activity levels with high transaction values. This trend is expected to continue in 2025, with nine deals completed in the first two months of the year. If this pace continues, 2025 is projected to see approximately 54 transactions and $22B in deal value (based on annualized figures). While the deal value might be slightly below 2024 levels, the total number of deals in 2025 is expected to be higher than 2024.

Despite the generally positive outlook, U.S. tariffs on Canadian energy and other goods (and Canada’s proposed retaliatory tariffs) are clouding deal forecasting for 2025. Defensive acquisitions will likely increase as dealmakers seek to shield themselves from a potential market downturn in response to the tariffs. Furthermore, recent investment policies from both countries—an “America First” investment policy from the U.S. and a stricter foreign investment review policy from Canada—present additional variables that could further impact transactions this year. As these developments continue to unfold, dealmakers will need to cope with a higher level of uncertainty in their market dealings.

Figure 1: Transactions involving Canadian infrastructure projects

Megadeals: small in volume but mighty in value

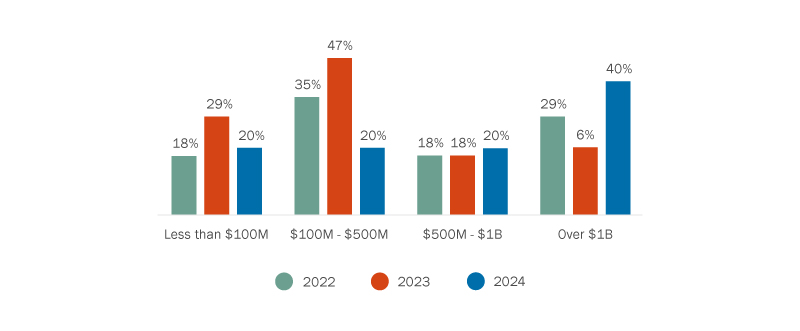

2024 saw a higher-than-usual proportion of large transactions, with over 40% of deals valued at over $1B. However, deal value is skewed by a small number of megadeals, largely driven by Neoen’s acquisition by Brookfield and Temasek, valued at approximately $14B. This trend towards megadeals is likely to continue throughout 2025, as illustrated by CDPQ’s $10B deal to buy Innergex Renewable Energy Inc. (Innergex), which was announced in February.

Four industry trends to watch

1. Renewables remain in focus

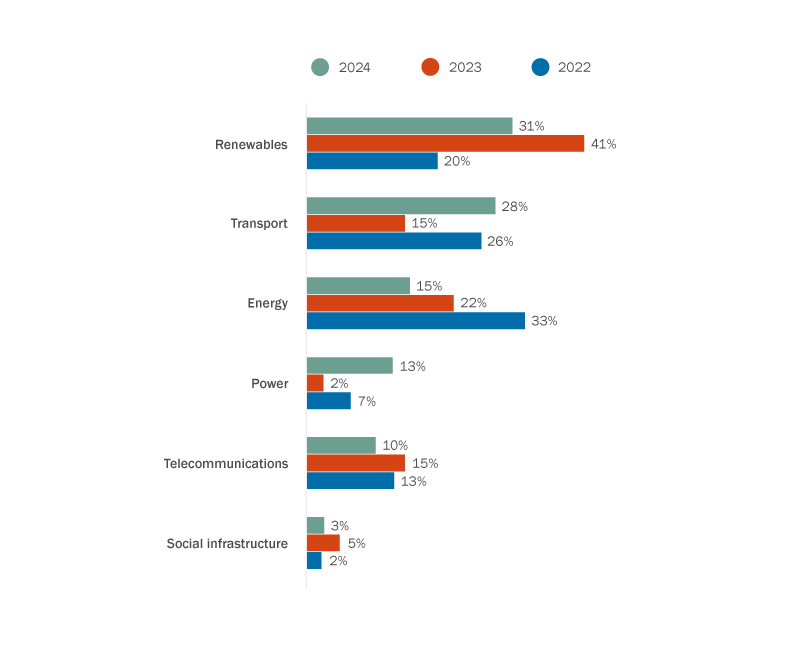

Renewable deals continue to lead the infrastructure M&A space in Canada, accounting for 31% of all deals in this space in 2024, though this represents a decline from 41% in 2023. The country’s continued efforts toward electrification are sustaining tailwinds for this sector despite pushback on renewable energy from south of the border. Innergex’s CEO commented that renewables still have a role to play in the long run, and that the market outlook in Canada is “very favourable”1. In addition to Innergex, two other renewable deals have been announced at the start of 2025: (1) Sitka Power Inc.’s acquisition of a portfolio of operating renewable electricity generation and battery energy storage assets from Saturn Power Inc. and (2) Connor, Clark & Lunn Infrastructure’s acquisition of a significant interest in the 180 MW Armow Wind and 149 MW Grand Renewable Wind projects in southern Ontario from Pattern Energy Group LP.

Figure 2: Infrastructure deal activity by industry

2. Data centres

Globally, data centre deals have been a high area of focus for dealmakers, and Canada is no exception. The growth of data centre projects is expected to increase steadily over the coming years, and a recent report by the Independent Electricity System Operator (IESO) indicates that the addition of multiple Canadian data centre projects substantially increased the electricity demand forecast for 20252. Significant deal activity in the energy sector is already underway to support the proliferation of data centres, which is being encouraged, in part, by federal and provincial initiatives to attract investment in Canada’s digital infrastructure, particularly by Canadian pension funds. Notable investment activity in this space includes Equinix’s $15B joint venture with GIC and Canada Pension Plan Investment Board for xScale data centre portfolio development, and this year’s announcement that Pembina Pipeline Corp. is investing in a large natural gas power plant that could supply a massive data centre complex.

3. Transportation

There has been a 28% increase in activity in the transportation sector compared to previous years, covering rail, ports, roads and other subsector areas. Several large deals in 2024 demonstrated continued interest in these assets, including Cando’s acquisition of the Enterprise terminal, the Mobil Grain Ltd. sale to GCM Grosvenor, the acquisition of Montreal-based LOGISTEC Corporation Logistec, and the equity stake acquisition of QSL International Ltd., among others.

4. Transmission and distribution

We expect to see continued interest in transmission and distribution assets in 2025 as demand for electricity continues to grow. To meet these rising demands, Canada and its provincial governments are looking to encourage investment in its transmission and distribution infrastructure. Notable transactions in this space include the following:

- Ontario’s Hydro One has four major transmission projects planned, and in 2025, they completed the acquisition of an approximately 48% interest in the East-West Tie Limited Partnership from affiliates of OMERS Infrastructure Management Inc. and Enbridge Transmission Holdings Inc. The East-West Tie Limited Partnership owns the East-West Tie Line, a 450-kilometre, 230kV double-circuit transmission line regulated by the Ontario Energy Board, which spans from Wawa to Thunder Bay along the north shore of Lake Superior.

- In September 2024, Axium Infrastructure announced that one of its managed funds had acquired an 80% equity interest in PUC Transmission LP, a regulated transmission utility established to construct and operate a greenfield transformation station and transmission line project located in Sault Ste. Marie, Ontario. The project will comprise a 10-kilometre, 230kV double-circuit transmission line and a 230kV transformer station, powering (among other connections) Algoma Steel Inc.’s transition to using electric arc furnaces to reduce its CO2 emissions.

The continued prominence of platform deals

Figure 3: Deal value ranged for transactions involving Canadian infrastructure projects

2024 saw a significant increase in deals valued at over $1B, which reflects a continued focus in the infrastructure and energy sector on platform deals. Infrastructure and energy investors are shifting focus from one-off plays to platform growth, as many are looking to acquire or finance companies with a pipeline of assets. The previously mentioned $10B Innerjex deal indicates that 2025 will likely continue this trend of buyers snapping up platform assets, and this activity will likely drive higher deal values.

Building on the momentum for infrastructure and energy M&A

We expect infrastructure and energy transactions to remain prominent in Canada’s M&A landscape. Data centres, transmission and distribution projects, and platform deals (especially in the renewables space) will drive continued deal activity for 2025, peppered by megadeals that will contribute to higher transaction values. As Canada looks to shore up its energy security and meet rising energy demands, dealmakers in this space will have ample opportunities to capitalize on the momentum in the sector.

- BNN Bloomberg, “Quebec pension fund manager to buy Innergex Renewable Energy in deal valued at $10 billion”, February 25, 2025.

- Independent Electricity System Operator (IESO), “IESO Releases Updated Demand Forecast”, October 17, 2024.

To discuss these issues, please contact the author(s).

This publication is a general discussion of certain legal and related developments and should not be relied upon as legal advice. If you require legal advice, we would be pleased to discuss the issues in this publication with you, in the context of your particular circumstances.

For permission to republish this or any other publication, contact Janelle Weed.

© 2025 by Torys LLP.

All rights reserved.